If you’ve been shopping for a home in Conroe, The Woodlands, or anywhere in North Houston lately, you’ve probably seen a mortgage buydown offer — things like “2.99% starting rate!” or “Builder-paid 2-1 buydown!” It sounds exciting — but what does it actually mean? And more importantly, is it a good deal for you? Let me explain it the same way I would sitting across from you at a kitchen table.

What Is a Mortgage Buydown?

A mortgage buydown is when someone — usually a builder or a seller — pays money upfront to reduce your interest rate. That money goes to the lender, who gives you a lower rate for either a set period of time or the life of the loan. There are two main types:- Temporary buydown: Your rate is lower for the first 1–3 years, then settles into a fixed rate for the rest of the loan. This is what most builders are offering right now.

- Permanent buydown: Your rate is lower for the entire loan term. This is also called “buying points.” It costs more upfront but saves money every single month.

How a 2-1 Buydown Works

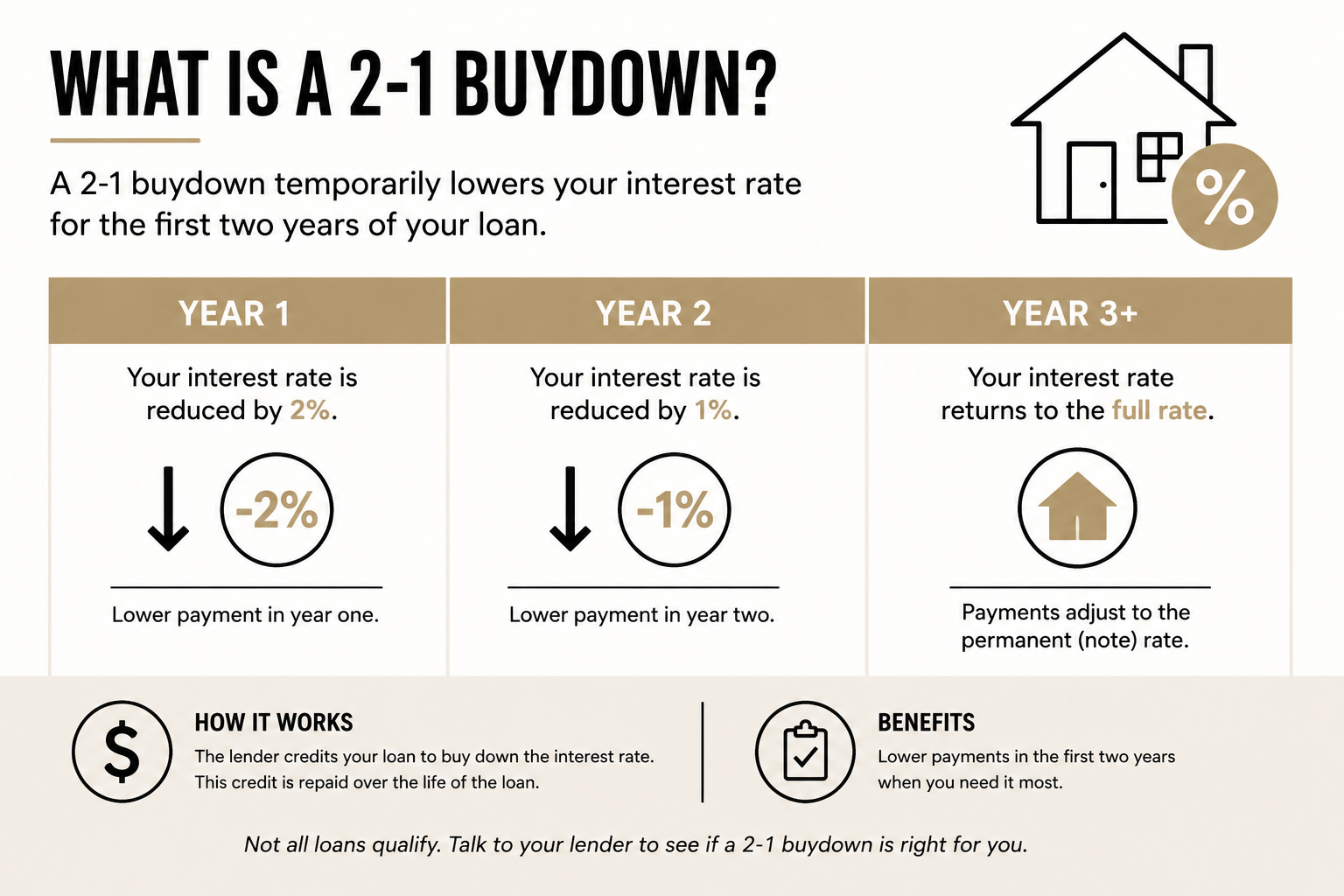

The name tells you the structure. In a 2-1 buydown, your rate is reduced by 2 percentage points in year one and 1 percentage point in year two. Then it locks into the note rate for years 3 through 30. Here’s a real example from Coventry Homes at Westridge Cove in Conroe, which is currently offering this incentive on their new construction homes:- Year 1: 2.99%

- Year 2: 3.99%

- Year 3 through 30: 4.99% fixed

Who Pays for the Mortgage Buydown?

Here’s the part that surprises most buyers: you usually don’t pay for it. The builder or seller covers the cost of the buydown as a concession. They’re essentially pre-paying a chunk of your interest to the lender so you get a lower payment out of the gate. Why would a builder do that? Because it’s a powerful marketing tool. They can advertise a rate starting near 3% while keeping their list price where they want it. You get lower payments in the early years. Both sides benefit — as long as you understand what you’re agreeing to. If you’re buying resale and negotiating with a seller, a buydown can also be structured as part of a seller concession at closing. The seller credits you money that goes toward the buydown fund at your lender. This is becoming more common in resale negotiations across Montgomery County as well.Is a Buydown a Good Deal?

That depends on your situation. Here are the honest factors to weigh:When it makes a lot of sense

- You’re a first-time buyer with a tighter budget and need lower payments in your first year while you adjust

- You’re relocating and waiting for another home to sell — the lower initial payment gives you cash flow flexibility

- You believe rates will drop in the next 1–2 years and plan to refinance before the rate fully resets

- The long-term locked rate (like 4.99%) is significantly below current market rates — locking in a below-market rate forever is a real, lasting benefit

When to be cautious

- If the long-term rate after the buydown period is only slightly better than what you’d get elsewhere — that first-year rate looks better on paper than it is in practice

- If the builder is rolling the cost of the buydown into a higher home price — you may be paying more for the home than it’s actually worth

- If you plan to refinance in year one — you could lose the unused portion of the buydown fund

Questions to Ask Before You Accept a Buydown

Before you let a 3% starting rate close the deal, ask these questions:- What is the fixed rate after the buydown period ends?

- What is the APR (annual percentage rate) on this loan — not just the starting rate?

- Am I required to use the builder’s lender? What are their fees?

- Is the buydown cost factored into the purchase price of the home?

- What happens to the buydown fund if I refinance early?

Mortgage Buydown Options for North Houston Buyers Right Now

We’re in a market where builders have inventory to move and buyers are sensitive to monthly payments. That combination has produced some of the most aggressive financing incentives we’ve seen in years — and buydowns are the centerpiece of most of them. If you’re shopping for new construction in Conroe or North Houston, a builder-paid buydown is absolutely worth factoring into your decision. Just make sure you understand the full picture — not just the headline rate. The right move is the one that fits your timeline, your budget, and your long-term plans. Some communities I’ve reviewed that are currently offering competitive incentives:- Coventry Homes at Westridge Cove — new construction under $300K in west Conroe

- Perry Homes at Woodlands Hills — established master-planned community in North Houston

- Grand Central Park — resort-style amenities along I-45